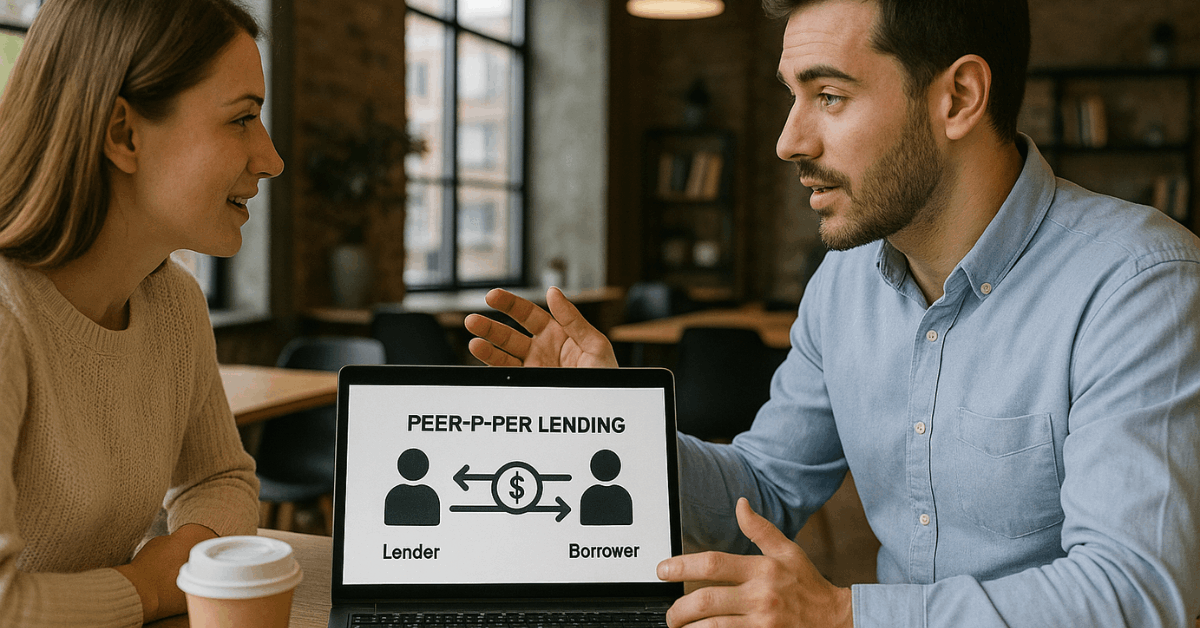

Peer-to-peer lending has become a modern solution for both borrowers and investors. Understanding how peer-to-peer lending platforms work helps you make informed financial decisions.

These online systems connect people directly, eliminating traditional banks as middlemen. This article explains their structure, benefits, and what you should know before joining one.

What Peer-to-Peer Lending Means?

It allows individuals to borrow and lend money through digital platforms. The process is simple but powerful, giving borrowers access to funds and investors a chance to earn interest.

These platforms act as intermediaries that manage risk and automate transactions. They are transforming how people handle borrowing and investing online.

How Peer-to-Peer Lending Platforms Operate?

To understand, you must know how the entire process flows from registration to repayment. Each stage is managed through secure digital systems that evaluate, match, and monitor loans efficiently.

- Registration and Verification: Borrowers apply online and undergo credit checks, while investors create accounts to fund loans.

- Listing and Funding: Approved borrowers are listed on the platform, allowing investors to choose who to lend to.

- Agreements and Disbursement: Once funded, contracts are signed, and funds are transferred electronically.

- Repayment and Returns: Borrowers repay in installments, and investors receive principal plus interest.

Technology Behind the Process

Modern P2P platforms like LendingClub and Prosper use algorithms and artificial intelligence to match borrowers and investors quickly.

They calculate risk scores, assign interest rates, and manage funds securely. This automation minimizes bias and speeds up approvals.

Types of P2P Lending

Different categories exist within this lending, each serving specific financial purposes. Understanding these options helps you choose the right platform based on your goals.

Consumer Lending

This is the most common type, where individuals borrow for personal expenses or debt consolidation. It’s a faster alternative to bank loans and often has competitive rates.

Business Lending

Small business owners use this option to finance operations or expansions. It provides access to capital for those who may not qualify for traditional bank loans.

Real Estate and Specialized Loans

Some platforms like Funding Circle and Mintos specialize in property, education, or short-term invoice financing. These niche categories attract investors looking for targeted opportunities.

Benefits for Borrowers

Borrowers often turn to P2P platforms because of accessibility and flexibility. Compared to traditional banks, they can enjoy easier processes and customized loan terms.

- Faster Approvals: Online systems reduce waiting time for loan approvals.

- Competitive Interest Rates: Rates are generally lower since there’s no banking intermediary.

- Flexible Repayment Terms: Borrowers can choose payment schedules suited to their income.

- Improved Credit Opportunities: Responsible repayment can build a better credit profile.

Benefits for Investors

Investors use P2P lending to earn higher returns than typical savings accounts. The platforms offer control, flexibility, and transparency over investments.

- Higher Potential Yields: Returns often exceed those from bank deposits.

- Diversification: You can fund multiple borrowers to spread risk.

- Low Entry Barriers: Minimum investments are affordable for most people.

- Transparency: Platforms display borrower details and risk levels openly.

Risks and Challenges in P2P Lending

Every investment carries risk, and P2P lending is no exception. Knowing the potential downsides ensures smarter decisions.

- Default Risk: Borrowers might fail to repay, leading to loss of returns.

- Platform Risk: A company could shut down or face operational issues.

- Liquidity Limitations: It can be hard to withdraw funds before loan maturity.

- Regulatory Uncertainty: Legal protections differ by country and are still evolving.

Regulations and Consumer Protection

Governments are creating guidelines to make P2P lending safer. These rules help maintain fairness and accountability between users.

- Licensing Requirements: Platforms must register under financial authorities like the U.S. Securities and Exchange Commission (SEC) or UK Financial Conduct Authority (FCA).

- Transparency Rules: Operators must disclose borrower data and platform performance.

- Investor Safeguards: Funds are often held in escrow accounts for security.

- Regular Audits: Periodic reviews ensure compliance and prevent misuse.

Evaluating a P2P Platform

Choosing a reliable platform is critical for both borrowers and investors. A few checks can help you minimize risk and ensure a better experience.

What to Check Before Joining?

Verify the company’s registration and regulation status.

- Review its default rate and historical loan performance on sources like CrowdRating.

- Read user feedback and independent reviews.

- Check its data security and privacy policies.

- Confirm withdrawal and repayment options before investing.

Expert Tips for New Users

Whether you’re borrowing or investing, success in P2P lending depends on discipline and strategy. Following best practices ensures safer and more rewarding experiences.

- Start small to test how the system works.

- Diversify your loans to lower risk exposure.

- Read all agreements carefully before funding or borrowing.

- Keep track of returns or payments using platform dashboards.

Stay informed about regulatory updates in your region through sources like OECD reports.

The Future of Peer-to-Peer Lending

The industry continues to evolve with new technologies and broader access. P2P lending is becoming more integrated with global finance systems.

Innovation Ahead

Artificial intelligence and blockchain will make transactions more transparent and secure. Cross-border lending may soon allow global investors to fund loans anywhere. As the market grows, competition will drive down costs and improve services.

Long-Term Outlook

The future of P2P lending points to more regulated and efficient systems. Stronger data protection and transparency will increase user confidence.

Better global standards will help create safer participation for everyone. As automation advances, costs will go down and services will improve.

These updates will expand access and strengthen the industry. Overall, P2P lending is expected to become a stable part of the global financial system.

Frequently Asked Questions

Here are some quick answers to help clarify common doubts about P2P lending.

- Is it safe? It’s relatively safe if you choose reputable, licensed platforms.

- Can I lose money? Yes, there’s always a small risk if borrowers default.

- How much can I invest? Minimum amounts vary but usually start low.

- Do I need to pay taxes? Returns are typically taxable as investment income.

Smart Takeaway

Learning how peer-to-peer lending platforms work helps you navigate modern finance confidently. These platforms provide equal opportunities for lenders and borrowers to benefit outside the banking system.

With the right precautions, you can use them to build wealth or access affordable credit. Make decisions wisely and treat P2P lending as a strategic part of your financial growth.